Trial pricing options are available for interested parties to subscribe and get access to the Outdoor Market Intelligence Service (OMIS). OMIS offers in-depth insight into the specialist and generalist outdoor retail market, with analysis available down to model level. Interested parties can access the strategy-shaping sell-through data from just €1,000 per month.

Now embedded in over 2,000 physical sales locations as well as online sales across the UK, DACH, and France, OMIS is the largest data service ever operated by and for the outdoor industry.

The service captures and tracks:

- Over 10 million unique SKUs, with new products added every month.

- Over 1000 brands.

- Over €7b of sales value.

Subscribers are already reporting that the tool is entrenched as part of their strategic decision making, monthly reporting and benchmarking. For brands, it supports product development, marketing positioning, pricing, while retailers get insights to support better buying and stock management. For both, it provides a near real-time barometer on performance as the market changes and evolves as well as a way of identifying market opportunities in time to capitalise on trends and patterns.

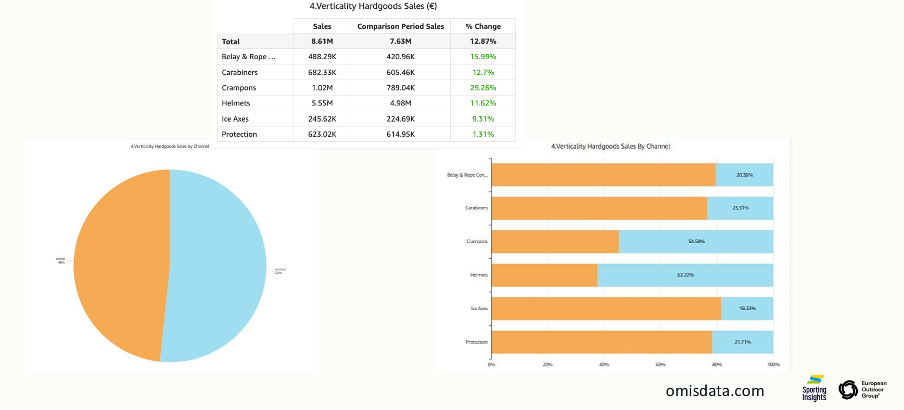

Results were recently shared with the industry at the recent European Outdoor Week, where a presentation by Marc Anderman and the EOG’s Hannah Piatok took attendees through Q1 2026 data at an overall level. They then took a deeper dive into verticality sales, a category that outperformed the market between January and March 2026.

While verticality remains a relatively small part of the overall market (€14m of the €317m total sales tracked in DACH for Q1, it was by far the fastest grower in Q1 (+9%). Hardgoods accounted for the largest growth within the category (+13%). This is good news for bricks and mortar retailers, with over half of these sales in-store in a corner of the market (verticality) where 60% of all sales are online.

Looking through a wider lens, the data shows that Petzl enjoyed a particularly good year in DACH in the full-year 2025, a 30% growth in sales turning its share into a market leading one.

Brand and own model level data is available to subscribers to the service.

As summer arrives, one area of interest will be camping sales, which traditionally spike between May and August, while in Autumn a focus will be premium apparel. Apparel, which accounts for over half of market value sales in DACH, declined slightly in 2025.

To sign up for the trial or for more information, please contact marc.anderman@sportinginsights.com

For more information visit www.omisdata.com

OMIS was created by and for the outdoor industry in collaboration or partnership with the European Outdoor Group (EOG). It is supported by major brands and retailers and endorsed by trade federations including: Outdoor Industries Association (OIA), Outdoor Sports Valley (OSV), OUTTRA, The Association of Sporting Goods Producers and Sports Equipment Suppliers in Austria (VSSÖ) and Snowsports Industries America (SIA).